In India, the Goods and Services Tax (GST) has directed a profound transformation in taxation. A crucial aspect of GST compliance for businesses is the submission of various returns. Among these returns is the CMP-08, specifically tailored for Composition Scheme taxpayers. This article serves as a comprehensive guide for comprehending and submitting the CMP-08 return. We provide complete guidance on the filing procedure and the relevant filing form required to file every quarter’s CMP 08 due date under the GST Composition Scheme for the upcoming months.

For Composition Scheme dealers, Form CMP-08 serves as a distinctive statement and payment form. It is used to report their self-assessed tax liabilities for a particular quarter and facilitates the tax payment process.

In April 2019, the updated tax payment procedure was introduced to streamline compliance for composition dealers. Form CMP-08 debuted in April 2019, becoming applicable from the fiscal year 2019-2020 onwards. It substituted the previous quarterly GSTR-4 filing method utilized by composition dealers.

Comprehensive Guide to the Filing Procedure of CMP 08. For Click here

What is Form GST CMP-08?

CMP-08, also recognized as the ‘Self-Assessed Tax Payment Statement,’ is a mandatory filing requirement for taxpayers operating under the Composition Scheme within the Goods and Services Tax (GST) framework. The Composition Scheme is tailored for small businesses with an annual turnover not exceeding Rs. 1.5 crore, offering them reduced GST rates and simplified compliance protocols.

A composition dealer, duly registered for both the supply of goods and services, must submit this return by the 18th of the month following the close of the respective quarter. Alongside Form CMP-08, a composition dealer is also obligated to furnish their annual return through the revised version of Form GSTR-4 by the 30th of April after the conclusion of the fiscal year.

Who Needs to Submit CMP-08?

The obligation to file CMP-08 rests with businesses that are eligible for the Composition Scheme. To be eligible for this scheme, a business must satisfy the following conditions:

The supplier of goods, which includes manufacturers and retailers, with an annual aggregate turnover of up to Rs. 1.5 crore (or Rs. 75 lakhs for special category States, except for Jammu & Kashmir and Uttarakhand) in the preceding financial year, unless:

- Manufacturer of ice cream and other edible ice (whether or not containing cocoa)substitutes.

- A person making interstate supplies.

- A person supplying goods that are not taxable under the GST Law.

- A casual taxable person or a non-resident taxable person.

- Businesses that supply goods through an e-commerce operator.

The supplier of services who meets the conditions cited under Notification Number 2/2019 Central Tax (Rate) on 7 March 2019 has an aggregate annual turnover of up to Rs.50 lakh in the previous financial year.

Read Also: GSTR 4 Annual File Due Date (Composition Taxpayers)

Following Are the Features of CMP-08

CMP-08 serves as a summary return, highlighting the following key features:

- Self-assessed tax payable information.

- GST liability payment for the quarter.

- Details on the composition scheme.

CMP 08 Due Date Quarterly For January to March 2026

| Period (Quarterly) | Due Dates |

| 1st Quarter – April To June 2025 | 18th July 2025 |

| 2nd Quarter – July To September 2025 | 18th October 2025 |

| 3rd Quarter – October to December 2025 | 18th January 2026 |

| 4th Quarter – January to March 2026 | 18th April 2026 |

Interest Applicable to Late Payment of GST CMP 08

For example, a missed taxpayer collects 100018/1001/365 = Rs. 0.49 for a single day, under which the fluctuation is grounded on the final payable tax & total days missed.

Filing Process For CMP 08 Form

All individuals registered under the GST (Goods and Services Act) of 2017, falling within the ambit of Section 10 of the CGST Act 2017, or those who have chosen to avail themselves of the benefits outlined in Notification No. 2/2019-Central Tax (Rate) dated March 7, 2019, are regarded by the Central Board of Indirect Taxes and Customs (CBIC) as a distinct category of taxpayers.

The CBIC has established a comprehensive protocol for the submission of returns, as stipulated in Notification No. 21/2019 – Central Tax, dated April 23, 2019. These assessments are conducted within the framework of the government’s composition scheme.

All individuals encompassed by the composition scheme are obligated to file CMP-08 every quarter. The due date for submitting returns for a given quarter is the 18th of the subsequent month following the conclusion of that quarter. For instance, the deadline for filing CMP-08 returns for the October to December 2023 quarter is January 18, 2023.

CMP 08 – A Move Widely Appreciated

CMP-08 is a statement cum challan that seeks information about outward supplies and inward supplies (inward supplies under reverse charge), including the taxes paid on such outward supplies and imports, along with the interest payable. CMP-08 is a welcome move, which was initiated in April 2019 so that it can be used from the financial year 2019-2020.

Latest Update & Notification

06th July 2022 – The GST dept has extended the due date of furnishing the GST CMP-08 quarter form till 31st July 2022 for the 1st quarter of FY 2022-23 via central tax notification number 11/2021. Read Notification

47th GST Council Meeting 29th June 2022 “To extend the due date of filing of FORM GST CMP-08 for the 1st quarter of FY 2022-23 from 18.07.2022 to 31.07.2022.” Read Press Release

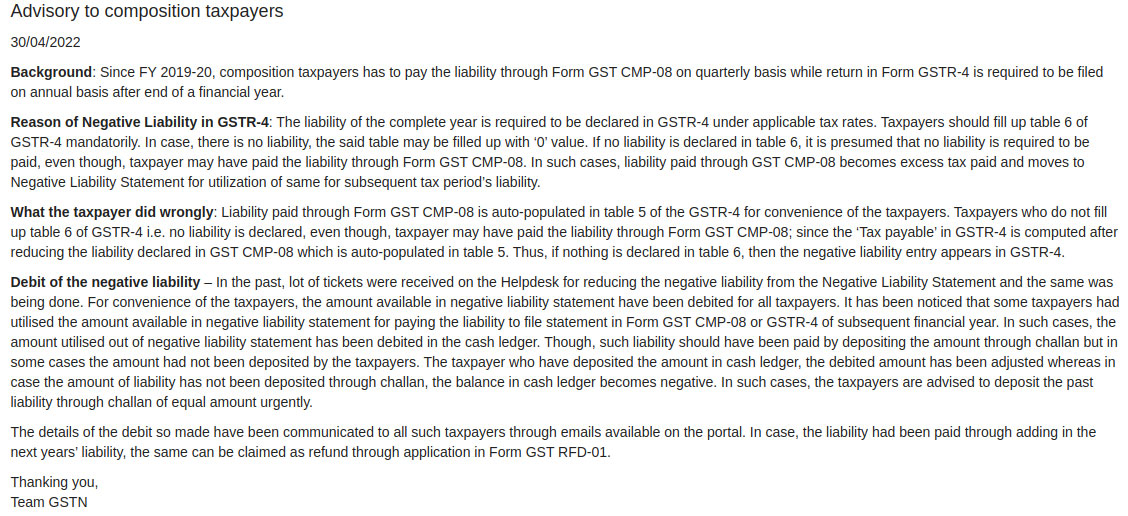

02nd May 2022– “The GSTN department has released a GST CMP-08 form advisory.” View More

{kind=link}

05th May 2021 – “CBIC notified the new notification for waiver of interest and a late fee for returns monthly or quarterly basis and composition taxpayers.” Read Notification

28th May 2021 – “NIL rate of interest for first 15 days from the due date of furnishing the statement in CMP-08 by composition dealers for QE March 2021, and reduced rate of 9% thereafter for further 45 days” Read 43rd GST Meeting PR

Penalty for Delay in Filing Returns under CMP 08

What are the consequences of failing to submit CMP-08 by the prescribed deadline?

When a taxpayer neglects to file their statement on or before the due date, they will incur a late fee of Rs. 200 per day for each day of delay. This amounts to Rs. 100 per day under CGST and Rs. 100 per day under SGST. The IGST Act mandates a late fee equal to that of the CGST and SGST Acts, i.e., Rs. 200 per day for each day of delay. These late fee charges are capped at a maximum of Rs. 5,000, calculated from the original due date to the actual filing date of the taxpayer.

It was furthermore, failing to submit CMP-08 for two consecutive quarters results in the blocking of e-way bill generation. To have the e-way bill generation unblocked, taxpayers must submit an application to their jurisdictional tax authority using Form GST EWB 05. Additionally, they may be required to complete all pending forms for previous quarters.