The validation parameters have been changed by the UDIN (Unique Document Identification Number) Directorate of the Institute of Chartered Accountants of India (ICAI), and expanded the data needed during UDIN generation under the ‘GST & Tax Audit’ and ‘Audit & Assurance Functions’ categories.

The ICAI has issued clarifications for the execution of a ceiling on tax audit assignments via the UDIN system. Under the newly issued FAQs, a maximum limit of 60 Tax Audit assignments per financial year per member will apply for UDIN generation w.e.f April 1, 2026.

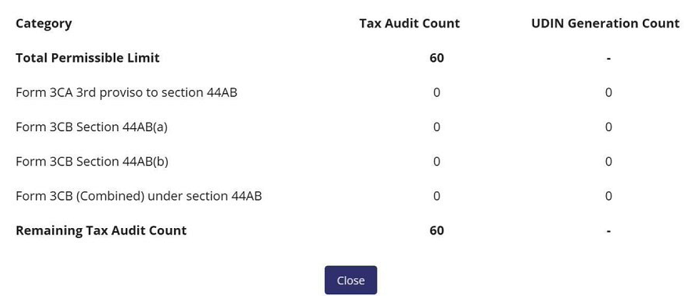

ICAI Introduces Tax Audit Count Tracking on UDIN Portal

A dedicated Tax Audit Count Dashboard has been rolled out by the ICAI UDIN Portal, which allows members to track their tax audit assignments and UDIN generation status in real time.

This newly inserted feature furnishes a consolidated view of the tax audit ceiling mentioned u/s 44AB of the Income-tax Act and assists practitioners in keeping track of audits organised under different reporting categories.

Demonstration of the new dashboard

The dashboard exhibits:

- Total Permissible Tax Audit Limit

- Tax Audit Count under various forms and clauses

- UDIN Generation Count corresponding to each category

- Remaining Tax Audit Count available to the member

The portal automatically computes the remaining audit capacity, assisting members in ensuring compliance with ICAI’s specified tax audit limits.

Importance of this feature

For practising chartered accountants, the tax audit limits are a constant compliance requirement. Maintaining track of assignments across various clients can be difficult in the peak tax audit season.

The new dashboard provides various advantages.

- Real-time monitoring of tax audit assignments

- Better compliance management with audit ceilings

- Improved transparency in UDIN-linked tax audits

- Reduced risk of exceeding permissible audit limits

- Easy verification before accepting new tax audit engagements

FAQs on Ceiling for UDIN Generation under Tax Audit

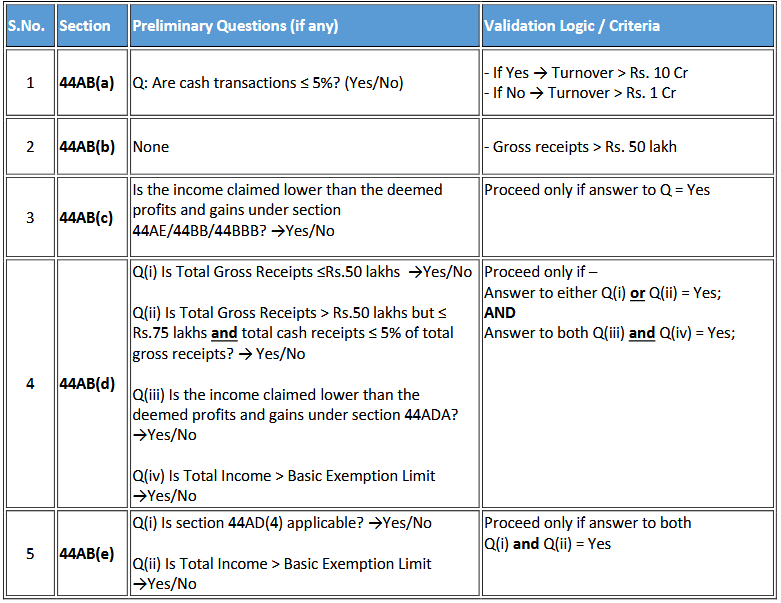

For execution of the ceiling on tax audit assignments via the UDIN system, only specified sub-categories under “GST & Tax Audit” will be acknowledged for computation of the ceiling. The ceiling on Tax Audit assignments is 60 per financial year per member and is applicable w.e.f. 1st April, 2026. It is controlled by the “Chartered Accountants (Limit on Number of Tax Audits) Guidelines, 2025” as published in the Gazette of India, which is available at Annexure I.

Key definitions

Applicable sub-categories: It shows the following sub-categories on which the ceiling shall be applicable:

- Form 3CA – 3rd proviso to section 44AB

- Form 3CB – Section 44AB(a)

- Form 3CB – Section 44AB(b)

- Form 3CB (Combined) under section 44AB

Non-applicable sub-categories: It signifies all other sub-categories u/s 44AB except the above specified sub-categories:

- Form 3CB – Section 44AB(c)

- Form 3CB – Section 44AB(d)

- Form 3CB – Section 44AB(e)

FAQs on Ceiling for UDIN Generation under Tax Audit are mentioned as

Q1. What is the ceiling on Tax Audit assignments for UDIN generation?

During UDIN generation under tax audit, a ceiling of 60 assignments per fiscal year per member shall be applicable.

Q2. How is the ceiling of Tax Audit assignments calculated?

As per the date of signing of the tax audit report, the ceiling will be calculated in the fiscal year and not on the date of UDIN generation.

Q3. Which sub-categories are regarded for the Tax Audit ceiling?

Under the applicable sub-categories, UDINs generated will be acknowledged for the ceiling.

Q4. Whether Tax Audit assignments undertaken in different firms or in individual capacity are aggregated?

Yes, the UDIN system will aggregate all Tax Audit UDINs generated by a member, whether in individual capacity or as a partner in one or more firms, for the ceiling.

Q5. Whether the UDIN generated for revised Tax Audit Reports is counted within the ceiling?

No, UDINs generated for the revised tax audit reports will not be considered as separate assignments for the objective of ceiling.

Read Also: ICAI Unveils Latest Edition of the Income-tax Act, 2025

Q6. How are UDINs for Head Office and Branch audits considered for ceiling objectives?

Audits for the head office and branches of the same taxpayer within the same assessment year will be counted as one Tax Audit assignment when generating a UDIN under the applicable sub-categories. However, the ceiling count will remain the same, even if multiple UDINs are issued.

Q7. How are multiple assessment years for the same taxpayer treated?

Under the applicable sub-categories, UDINs generated for different assessment years for the same taxpayer will be considered as separate assignments.

Q8. How are multiple forms for the same taxpayer treated?

Under the applicable sub-categories, multiple UDINs generated for the same taxpayer and the same assessment year shall be considered as one assignment.

Q9. What is the treatment of UDINs for Tax Audit assignments under various scenarios?

Under the norms specified in Annexure I, the treatment of UDINs generated for

Tax Audit forms/reports are as follows:

| S. NO. | Scenario / Description | Treatment of UDIN for Ceiling |

| 1 | UDINs generated for the same taxpayer under multiple forms within the applicable sub-categories | No additional count shall be made, given that the audits related to the same PAN and the same assessment year |

| 2 | Revision in the sub-category from a non-applicable sub-category to an applicable sub-category | The assignment shall be counted towards the ceiling and the available limit shall be reduced. |

| 3 | Revision in the sub-category from the applicable sub-category to the non-applicable sub-category | The assignment shall be excluded from the ceiling, and the available limit shall surge accordingly. |

Read the official Addendum to FAQs on UDIN Ceiling for Tax Audit: Click here

Taxpayer’s Permanent Account Number (PAN) will now be a mandatory field for UDIN generation under the ‘GST & Tax Audit’ category. While PAN will be mandatory during UDIN generation, the information will remain confidential and will not be seen by any third-party verifier.

Based on the following five parameters, the e-Filing Portal of the Central Board of Direct Taxes (CBDT) will now validate UDINs

- Membership Registration Number (MRN)

- UDIN

- Assessment Year/Financial Year (AY/FY)

- Form Number

- PAN of the taxpayer

ICAI, in a separate communication issued on the same day, obligated additional disclosures during UDIN generation under both ‘GST & Tax Audit’ and ‘Audit & Assurance Functions’ categories.

Succeeding auditors shall be needed to capture information about the preceding year’s audit while generating UDINs. The data provided by members on the same concern has been categorised as confidential and shall not be disseminated.

The decision was made at the Council’s 442nd meeting, held from 26th to 27th May 2025, and is indicative of the Institute’s efforts to strengthen audit trail mechanisms and improve accountability in statutory reporting.

ICAI has rolled out field-level validation for all sub-categories u/s 44AB. The council has determined to impose a ceiling on UDIN generation in alignment with the specified limit of 60 tax audits, with the cap becoming effective from 1st April 2026 for specified Forms, along with 3CA and 3CB.

Via communication with the UDIN Directorate at udin@icai.in, members can seek clarifications on any of the releases.

Official release of the notification by ICAI: Click here